Why Is There Such a Large Difference?

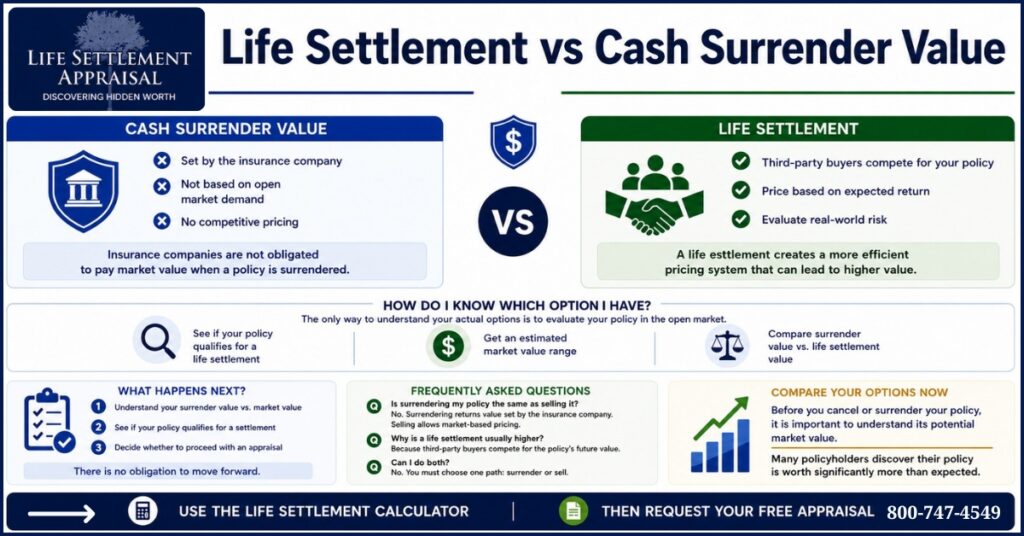

Insurance companies are not obligated to pay market value when a policy is surrendered.

A life settlement, however, allows third-party buyers to:

- Compete for your policy

- Price based on expected return

- Evaluate real-world risk

This creates a more efficient pricing system for many policyholders.

When Does Surrendering Make Sense?

Surrendering may make sense if:

- The policy has very low or no market value

- You do not qualify for a life settlement

- You need immediate cancellation simplicity

However, many policyholders choose surrender without realizing other options exist.

When Does a Life Settlement Make More Sense?

A life settlement may be better when:

- The policy has significant market value

- Premiums are no longer desirable

- Coverage is no longer needed

- Retirement liquidity is a priority

Check Your Eligibility Instantly

How Do I Know Which Option I Have?

The only way to understand your actual options is to evaluate your policy in the open market.

A structured review will show:

- Whether your policy qualifies for a life settlement

- Estimated market value range

- Whether surrender or sale is more advantageous

Use the Life Settlement Calculator

What Happens After I Check My Options?

Once you evaluate your policy:

- You understand your surrender value vs market value

- You see if your policy qualifies for a settlement

- You decide whether to proceed with an appraisal

There is no obligation to move forward.

Get a Free Life Settlement Appraisal

Frequently Asked Questions

Is surrendering my policy the same as selling it?

No. Surrendering returns value set by the insurance company. Selling allows market-based pricing.

Why is a life settlement usually higher?

Because third-party buyers compete for the policy’s future value.

Can I do both?

No. You must choose one path: surrender or sell.

What if my surrender value is low?

You may still qualify for a life settlement, which could provide significantly more.

Compare Your Options Now

Before you cancel or surrender your policy, it is important to understand its potential market value.

Many policyholders discover their policy is worth significantly more than expected.

Use the Life Settlement Calculator

Then Request Your Free Appraisal