Life Insurance Appraisal

Discover Your Hidden Worth

Discover Hidden Value in Life Insurance

What is A Life Settlement?

A life settlement is when you sell your life insurance for more than the cash value instead of just lapsing, canceling, or surrendering your policy. If you find your premiums are getting too high, you no longer need your life insurance or you do need cash to pay for the ever increasing costs of assisted living, a life settlement may be a good option. The purpose of this site is to educate you on the value you may have in your life insurance policy and to prevent consumers in general from just throwing away these valuable assets. Discovering hidden value in your life insurance policy starts with doing your homework. Get the value of your life insurance policy as a life settlement with a life settlement appraisal.

How Much Is Your Life Insurance Policy Worth?

Most life insurance policies sold in a life settlement receive between 10% and 40% of the policy’s face value, depending on age, health, policy type, and premium costs. Life Settlements are typically up to 6 times your existing cash value, but policies with no cash value and even term life insurance may qualify.

Use the Life Settlement Calculator to Estimate Your Value

Get Your Free Life Settlement Appraisal

How Much Is My Life Insurance Policy Worth?

The fastest way to estimate your policy’s value is to use our life settlement calculator.

Our proprietary calculator provides:

- A real-time value range

- Insight into whether your policy may qualify

- An estimate of potential payout

Most policies fall between 10% and 40% of face value, but your actual value depends on multiple factors. There is no way to accurately value a policy with a simple online life settlement calculator, but it will educate you as to which variables matter, give you an indication as to whether or not you are likely to qualify and give you an estimated range of value.

Estimate Your Policy Value Instantly

Can I Sell My Life Insurance Policy?

It really depends. Many life insurance policies can be sold if you meet age, health, and policy size requirements.

Policy owners often consider selling when:

- Premiums become too expensive

- Coverage is no longer needed

- Retirement income is needed

- A policy is about to lapse

Before submitting your policy, you can quickly check your likelihood of qualifying.

Check Your Eligibility with the Calculator

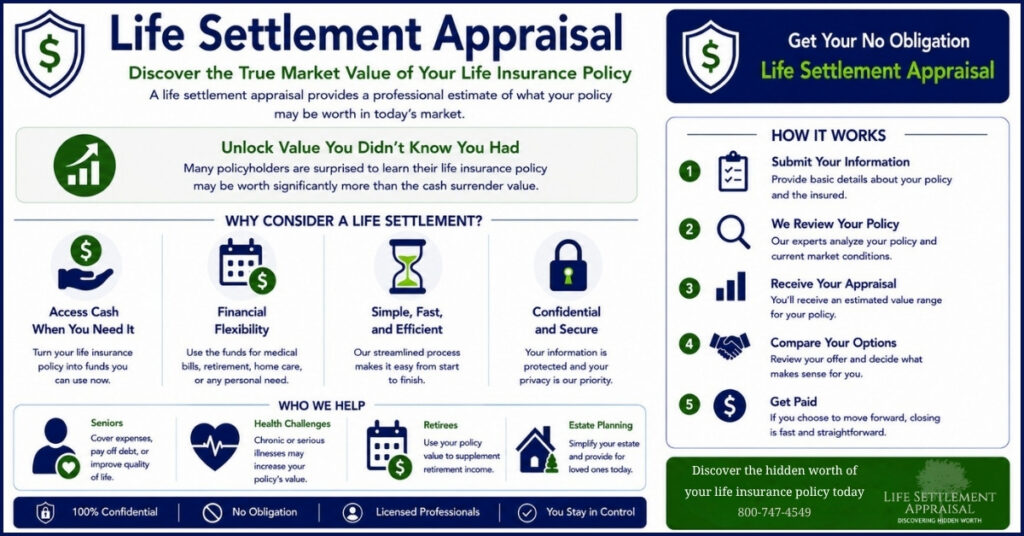

How Does a Life Settlement Appraisal Work?

A life settlement appraisal determines your policy’s market value range based on:

- Life expectancy

- Policy type

- Premium obligations

- Policy face value

Institutional buyers use this information to determine if they are willing to pay for your policy and how much your life settlement offer would be.

The best way to begin is to start with a calculator estimate to see if you are even likely to qualify, then request a full appraisal.

Start with the Life Settlement Calculator

What Is a Life Settlement Calculator?

A life settlement calculator is a tool that estimates the potential value of your life insurance policy using key factors such as age, health, and policy details.

It helps you:

- Understand what your policy may be worth

- See if you are likely to qualify

- Decide whether to proceed with a full appraisal

Estimate Your Policy Value Now

What Determines the Value of a Life Insurance Policy?

Several factors influence life settlement value:

- Age of the insured

- Health condition

- Policy size (face value)

- Premium cost

- Policy type (term, universal, whole life)

Key Insight: Higher age and declining health typically increase your policy value, while higher premiums may reduce or even eliminate any hidden value your policy may have.

Use the Calculator to Estimate Your Value

Who Qualifies for a Life Settlement?

Most life settlement buyers look for:

- Individuals age 65 or older

- Policies with face values of $100,000 or more

- Changes in health that impact life expectancy

Some term policies may also qualify if they are convertible. We’ve helped many people under age 65 sell their insurance policy, but they all had health impairments. If you are over age 65, you may qualify to sell your policy even if you are in perfect health.

Real Life Settlement Examples

Below are typical examples of life settlement outcomes. Actual values vary.

Example 1

Profile

- Gender: Male

- Age: 78

- Policy Type: Universal Life

- Face Value: $500,000

Situation

- Reason for Selling: Premiums became too expensive in retirement

- Existing Cash Surrender Value: $18,000

Outcome

- Estimated Life Settlement Value: $120,000

- Increase Over Surrender Value: ~6.5x

Example 2

Profile

- Gender: Female

- Age: 72

- Policy Type: Term (Convertible)

- Face Value: $250,000

Situation

- Reason for Selling: No longer needed coverage after children became financially independent

- Existing Cash Surrender Value: $0

Outcome

- Estimated Life Settlement Value: $45,000

- Value vs Surrender: Significant gain vs lapse

Example 3

Profile

- Gender: Male

- Age: 80

- Policy Type: Whole Life

- Face Value: $1,000,000

Situation

- Reason for Selling: Estate planning adjustment / liquidity needed

- Existing Cash Surrender Value: $95,000

Outcome

- Estimated Life Settlement Value: $300,000

- Increase Over Surrender Value: ~3x

Example 4

Profile

- Gender: Female

- Age: 69

- Policy Type: Universal Life

- Face Value: $750,000

Situation

- Reason for Selling: Change in health increased cost burden and reduced need for coverage

- Existing Cash Surrender Value: $40,000

Outcome

- Estimated Life Settlement Value: $210,000

- Increase Over Surrender Value: ~5x

Each policy and case is unique. The most accurate way to estimate your value is to use the calculator and then request a full appraisal.

See What Your Policy Could Be Worth

Is Selling a Policy Better Than Surrendering It?

In many cases, yes.

A life settlement can provide significantly more than the cash surrender value offered by the insurance company.

- Cash surrender value is typically the lowest payout

- Life settlements higher payouts by definition

Compare Your Options After Using the Calculator

Who Buys Life Insurance Policies?

Life insurance policies are purchased by:

- Institutional investors

- Life settlement companies

- Investment funds

These buyers evaluate policies as financial assets and determine value based on life expectancy and projected returns.

Sell Your Life Insurance Policy

Frequently Asked Questions

How much is my life insurance policy worth?

Most policies sold in life settlements receive between 10% and 40% of their face value. Use the calculator to estimate your specific range.

Can I sell my life insurance policy if I am healthy?

Possibly. Some policies may still qualify. The calculator can help determine your likelihood of qualifying.

What age qualifies for a life settlement?

Most buyers look for individuals over age 65, although younger individuals with certain health conditions may qualify.

Can I sell a term life insurance policy?

Yes. Some term policies can be sold if they are convertible or meet eligibility requirements.

Can I retain some death benefit, or must I sell the whole policy?

Depending on your health and policy size, a retained death benefit may be available. A retained death benefit gives you some cash now, eliminates future premiums, and reserves a portion of your death benefit for your beneficiaries.

Do I have to keep paying premiums after I sell my policy?

No, the buyer always pays premiums once your policy is sold and ownership transfers.

How long does a life settlement take?

Most transactions take a few weeks once all documentation is submitted. The initial estimate can be generated instantly using the calculator.

Free Life Settlement Appraisal

If you are considering selling your life insurance policy, the first step is understanding its value.

Start with the calculator to estimate your value and qualification, then submit your policy for a full appraisal. Appraisals cost nothing and there is never any obligation to sell your insurance policy.

Use the Life Settlement Calculator First

Then Request Your Free Appraisal

Life Settlement Loan

Depending on your health and age, you may be able to use your life insurance’s death benefit to get a loan or a line of credit allowing you an immediate cash advance before you die. Often there are no loan payments, premium payments, or interest to be paid while you are still living. Loans are sometimes possible even if living benefits or accelerated benefits are not an option in your case.

Viatical Settlements

A viatical settlement involves the sale of your life insurance policy once you have become chronically or terminally ill. a viatical settlement broker such as Life Settlement Appraisal has a fiduciary responsibility to you, the viator. Viatical brokers should shop your insurance policy to the highest bidding viatical providers that are licensed in your state.

Medicaid Life Settlement

A Medicaid Life Settlement is converting a life insurance policy for a pre-paid, Long Term Care Benefit Plan that covers the monthly burden of high care costs. A Medicaid Life Settlement is a unique financial option for seniors because there are no wait periods, no care limitations, no costs to apply, no requirement to be terminally ill, and there are no premium payments.

Understanding Better

The Right Questions

-

How Can a Life Settlement Provider Help You?

Life seldom works out as planned. A life settlement provider may be able to help you convert your life insurance policy to cash. Life settlement providers are companies, or sometimes individuals, who operate in the secondary market for life insurance. You should not confuse them with life insurance companies. They are in the business of aggregating and buying policies and do not have any fiduciary relationship with their…

-

Are There Any Taxes Associated with Life Insurance Settlements?

Life insurance settlements are a way to monetize a life insurance policy that is no longer wanted or needed. There are tax implications that must be considered. The ability to enter in a life settlement agreement has been legal for over 100 years. It was almost a well-guarded secret, as insurance companies would rather pay the insured the cash surrender value of his or her life insurance policy…

-

What are the risk factors for life settlement investments?

Life settlements bring together a willing seller and a willing buyer. As the policy owner, or seller of the life insurance policy, you know exactly what you are getting. When you negotiate and agree to a settlement with the life settlement provider, you receive an agreed amount in the form of a single lump sum. As the buyer of the policy, a life settlement company is making an educated guess…

-

What are Life Insurance Settlements?

Seniors should have life insurance policies evaluated by a professional before cashing them out for cash surrender value or just abandoning the policy. A life settlement company can help determine if the life insurance policy has hidden value.

Life Settlement Appraisal

"*" indicates required fields

Life Settlements Need to Know

- Life Insurance is an assest

- You can sell your life insurance to pay for long term care

- It is possible to use a life insurance policy to secure a loan

- Life Insurance can help you access liquid funds now

- Elders are discovering unexpected hidden value in their life insurance policies

- A medicaid life settlement can pay directly for in-home long term care or nursing home care

- A Life Settlement means no more high monthly premium payments

- Never surrender a life insurance policy without having an appraisal of it’s value